Andrey BabynininDataDrivenInvestorTesting trading strategy with ML and hammer candleThe article is around testing the predictable power of a well-known feature of technical analysis: hammer. Hammer at the end of the…5 min read·Apr 4, 2021----

Andrey BabyninNFT: a closer look (March 5–11)I week ago I decided to start tracking all the hype around NFT. For this purpose, I start to weekly monitor the top 100 positions on…2 min read·Mar 12, 2021----

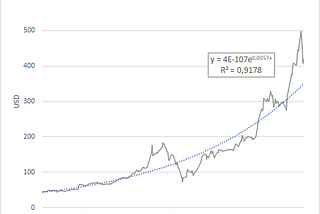

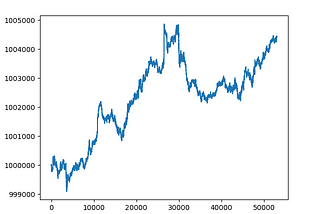

Andrey BabyninLog-periodic power law singularity model and Tesla stockIn this article I try to explain the basics of LPPLS model using Excel and Tesla stock.4 min read·Sep 7, 2020--1--1

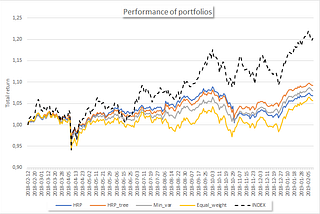

Andrey BabynininDataDrivenInvestorHierarchical Risk Parity in Portfolio ConstructionThis is a practical application of Marcos López de Prado articles (1 and 2) on portfolio optimization process. More specifically, I will…6 min read·Feb 26, 2020--1--1

Andrey BabyninReinforcement learning in Trading (part 2 - the last)In the previous post, I started to write about my trading RL experiment. Today I decided to complete the description of the trading…3 min read·Feb 6, 2020--1--1

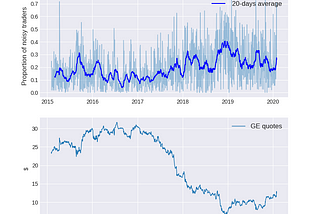

Andrey BabynininTowards Data ScienceHerding Model in Financial MarketsThis article is devoted to the herding mechanism in stocks.5 min read·Feb 1, 2020----

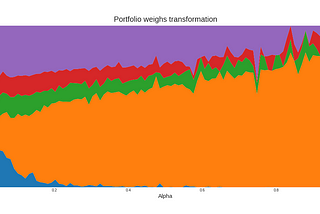

Andrey BabynininDataDrivenInvestorPortfolio optimization using particle swarm algorithmParticle swarm optimization is a kind of natural algorithms like genetic algorithms.4 min read·Nov 26, 2019--1--1

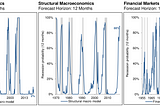

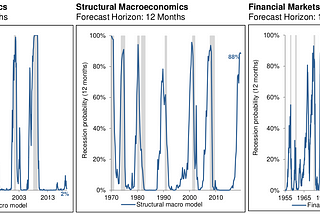

Andrey BabyninEconomic recession: how to count probabilitiesThis year I have come across several pieces of research and insights from investment firms and think-tank with estimates of recession…3 min read·Nov 25, 2019----

Andrey BabyninReinforcement learning in trading (Part 1)This is a brief introduction on how to make a simple bot for trading.3 min read·Aug 4, 2019--2--2

Andrey BabynininTowards Data ScienceETF2Vec: My story about trying to extact narrative from ETF holdingsThe world is occupied by embeddings models. Word2vec, Image to vectors and much more. After recent news about extacting knowledge from…5 min read·Jul 22, 2019----